Financial Analysis - FinExAnalysis 2012

New product

The main purpose of the program FinExAnalysis - to make the financial ana

The main purpose of the program FinExAnalysis - to make the financial analysis of organizations effective, convenient and prompt, including in conditions of limited time. You can use the developed system FinExAnalysis for:

- Constant quarterly monitoring of the financial condition of enterprises and organizations;

- Development of forecasted balances and forecasted financial results;

- Conducting an express analysis of the financial condition of the enterprise in a short time;

- Preparation of analytical notes to financial statements;

- Preparation of analytical materials for meetings of shareholders, members of labor collectives;

- Development of an enterprise development strategy in the medium and long term;

- Development of programs for the recovery of financial condition (sanitation) of enterprises for arbitration managers;

- Carrying out of regulated analyzes in accordance with regulatory acts of regulatory agencies;

- Conducting financial analysis during the audit;

- Identify possible options for further development of the enterprise by drawing up a matrix of financial strategies.

- The simple and convenient interface of the program Financial Analysis - FinEkAnaliz distinguishes it from other similar packages, which is noted by the majority of users. You do not have to spend long hours to develop the product. You will be able to receive the first report within half an hour after entering the financial statements.

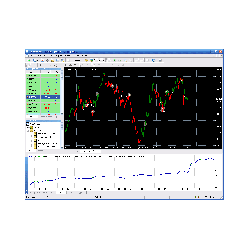

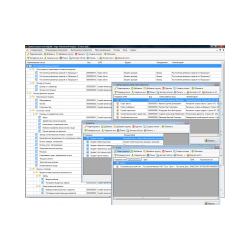

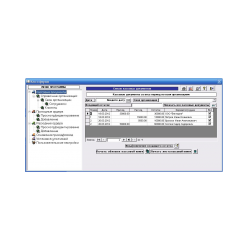

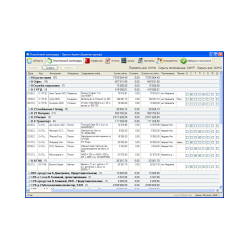

- Based on the financial statements (Form # 1, Form # 2 and, if necessary, Form # 3, Form # 4, Form # 5), the program generates analytical text reports along with graphical charts and recommendations for improving the financial condition.

- The results of the analysis are transported to MS Word, where they can easily be edited to your needs.

- An important feature of the program is the openness of the methods used by economic calculations for users.

- FinExAnalysis in the financial analysis program category is one of the best in terms of price / quality ratio. Our prices are several times lower than those of competitors while maintaining basic functionality. This was achieved by minimizing costs.

Related Products

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)